FTC Significantly Curtails Long-Awaited Changes to HSR Premerger Notification Rules and Procedures

Client Alert | 8 min read | 10.15.24

The Federal Trade Commission voted unanimously to pass a final rule implementing significant changes to the premerger notification regime under the Hart-Scott-Rodino (HSR) Act. The Department of Justice concurred with the vote. The final rule significantly reins back the agency’s proposed rule issued in June 2023—a proposal that would have imposed substantial new burdens on merging parties and prompted widespread criticism. The final rule is still the most significant overhaul of the HSR premerger notification requirements in decades, and the new requirements will impose additional time and expense on merging parties, some of which can be mitigated by putting processes in place in advance.

Key Takeaways

- The final rule scaled-back or outright rejected many of the most burdensome aspects of the proposed rule. Concurring statements by the two Republican Commissioners indicated that they would not have supported the final rule without these changes, and said that many aspects of the proposed rule would have exceeded the agency’s authority.

- The final rule imposes material changes to the premerger notification form and procedures, although the scope of the additional burden that these changes will have on merging parties will depend on certain factors, such as whether the parties have overlapping products or services, whether they have a supply relationship, or whether they are in industries that are uniquely affected by the new rules such as private equity.

- The final rule will not take effect immediately. Merging parties will continue to file under the current HSR system until the effective date of the final rule (unless challenged) which will be mid-January 2025.

- Parties can begin preparing for the new notification filing requirements now by implementing routine business protocols to facilitate efficient reporting processes.

Extensive Proposed Rule Changes Substantially Modified/Rejected in Final Rule

The final rule reflects the FTC’s consideration of public feedback, omits several burdensome requirements that were initially proposed, and likely reflects the compromise needed to achieve unanimous support among the five commissioners. See, e.g., Statement of Commissioner Melissa Holyoak (“Many of the [proposed] filing requirements, if implemented, would have been beyond the Commission’s legal authority, arbitrary and capricious, unjustifiably burdensome, and just plain bad policy. … I have worked to curb the excesses of the [proposed rule] in meaningful ways that would not have happened absent my support.”). Notably, the following proposals did not make it into the final rule:

- Detailed Labor Market Information: The original proposal included requirements for detailed disclosures about labor markets and employee information to assess potential labor market effects. The final rule excludes this requirement.

- Draft Documents: The FTC initially proposed requiring parties to submit drafts of Item 4(c) and 4(d) documents. The final rule only requires the submission of final versions of these documents.

- Prior Acquisitions: The proposed rule contemplated that merging parties would have to disclose substantially more information regarding prior acquisitions (e.g., ten-years lookback with no size limit). The final rule maintains the current five-year lookback period and $10 million de minimis exception, but expands the reporting requirement in other regards.

- Extensive Narrative Competitive Analyses: The proposed rule sought comprehensive narrative descriptions analyzing competitive overlaps and market conditions. The final rule instead requires only brief descriptions.

- Broad Disclosure of Non-Controlling Minority Investments: The initial proposal required extensive reporting on all minority investments and affiliations. The final rule narrows this to focus on entities with potential competitive overlaps or significant corporate control/management rights.

- Detailed Customer and Supply Relationship Information: The proposed rule mandated extensive details on customer and supplier relationships, including the submission of licensing agreements and non-compete clauses. The final rule scales back these requirements, focusing on the identification of significant supply relationships.

Noteworthy Modifications to HSR Form and Procedures Under Final Rule

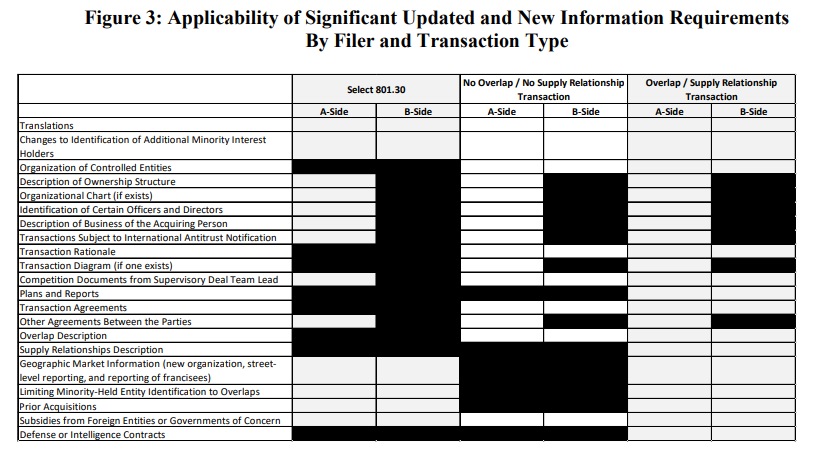

Despite scaling back some proposals, the final rule introduces several significant changes that will impact all HSR-reportable transactions. As noted in the diagram below, whether a notifying party must submit information under these new rules—and what information they will have to submit—depends on: (1) whether the transaction qualifies as a “Select 801.30 Transaction”[1]; (2) whether the transaction does or does not report a NAICS code overlap, described overlap, or a supply relationship; and (3) whether the notifying party is on the A-side (buyer) or B-side (seller) of the transaction.

The following are some of the most expansive and burdensome requirements that merging parties may have to comply with depending on the factors noted above:

- Expanded Scope of Required Documents

- Inclusion of Supervisory Deal Team Lead Documents: In addition to submitting Item 4(c) and 4(d) documents prepared by or for officers or directors, parties must now submit Item 4(c) and 4(d) documents prepared by or for the “supervisory deal team lead,” defined as the individual primarily responsible for supervising the strategic assessment of the deal who is not an officer or director.

- Regularly Prepared Plans and Reports: Filers must provide one year’s worth of certain “regularly prepared” high-level strategic business documents, not created in connection with the transaction, that discuss market shares, competition, competitors, or markets of any overlapping product or service, and that were shared with the CEO or Board of Directors.

- Drafts Shared with Board Members: If a draft document is responsive to Item 4(c) and 4(d) and was shared with any member of a Board of Directors, the document should not be considered a draft and must be included in the filing.

- Translations for Foreign-Language Documents: If a filing includes documents in a foreign language, filers must provide English-language transalations.

- Enhanced Transaction and Competitive Overlap Details:

- Description of Acquirers: Acquirers must provide a short description of their operating businesses and ownership structure, as well as information about jurisdictions outside the U.S. where competition filings have been or will be made.

- Product and Service Descriptions: Both parties must describe current or planned products and services that compete with or are related to those of the other party. The agency’s goal is to identify transaction that may lessen future, potential competition and innovation.

- Supply Relationships: Parties must disclose any supply relationships between the parties or with entities that compete with the other party, including a description of the products, services, or assets and associated revenues. The goal is to try to identify transactions that may harm non-horizontal competition.

- Revenue Data: Parties must provide revenue data for overlapping products or services for the most recent fiscal year. Parties must provide the same data for each product, service, or asset in which they have a supply relationship with the target or target’s competitor.

- Customer Information: Parties must describe categories of customers and list the top ten customers by units sold and sales revenue for overlapping or supply relationship products, services, or assets.

- Additional Background and Details Regarding Filing Parties

- Officer and Director Information for Interlocking Directorates: Acquiring persons must list their officers and directors and identify any third-party entities where these individuals hold positions that operate in the same industries as the target. This aims to facilitate the assessment of potential violations of Section 8 of the Clayton Act, which prohibits interlocking board directors and managers between competing corporations.

- Minority Shareholders and Affiliations: Filers must provide more detailed information about minority shareholders, investment funds, and entities holding indirect stakes, particularly those with management rights or competitive overlaps.

- Expanded Reporting of Prior Transactions: Both acquirers and acquired persons must report certain acquisitions made in the preceding five years, extending the requirement beyond just the acquiring person. This includes acquisitions of substantially all of the assets of a business.

- Disclosure of Defense and Intelligence Contracts: Acquirers will be required to disclose information about any defense and intelligence contracts generating more than $100 million of revenue, if there is an overlap or supply relationship.

- Disclosure of Subsidies from Foreign Entities or Governments of Concern: Parties must disclose any subsidies received within the two years prior to filing from foreign entities or governments designated as strategic or economic threats to the U.S., such as China, Iran, North Korea, and Russia.

- Ownership Structure Diagrams: Acquirers are required to submit organizational diagrams showing relationships between the ultimate parent entity and affiliates or associates involved in the transaction, if such diagrams exist in the ordinary course of business. Acquirers, however, are not obligated to create such diagrams from scratch.

Conclusion

The finalization of the new HSR premerger notification rules marks a significant shift in the obligations of reporting parties. While the FTC scaled back some of the more onerous proposals from the original draft, the new requirements will substantially increase the time and resources needed to prepare HSR filings, particularly where there is a product/service overlap, supply relationship, and for certain organizations, such as private equity funds. Parties exploring future transactions should:

- Review Document Creation and Retention Practices: Ensure that certain types of deal-related and strategic internal documents are prepared with the understanding that they may be among the first documents reviewed by regulatory agencies. In addition, good document retention processes among individuals who may have Item 4 documents, such as isolating deal-related documents and clearly marking drafts, will expedite later collection and review needed for filings.

- Implement Processes to Quickly Identify Necessary Information: Review areas of new information required to assess whether upgraded internal protocols may assist in efficiently gathering information when filings are prepared. Examples may include information about minority investors and fund structure, third-party positions held by officers and directors, and types of supply and other agreements in place with key industry participants.

- Begin Preparations Early and Build in More Time: The agency estimates that the average time required to prepare a filing will nearly triple, rising from 37 hours to 105 hours, with the new HSR requirements. Start gathering required information and documents earlier in the period before filing dates. Consider whether a “mock” HSR filing exercise focusing on the new requirements would be helpful to identify areas for streamlining or implementing new processes. Also, be mindful to update standard filing covenants in transaction agreements to account for the additional time necessary to prepare the filings.

- Consult Antitrust Counsel: Engage legal experts early to navigate the complexities of the new rules and to develop strategies to streamline the information collection process.

One positive development in connection with the FTC’s final rule is that the FTC also announced that it will reinstate the practice of granting early termination of the 30-day initial HSR waiting period once the final rule becomes effective. This could expedite deal timelines for transactions that do not raise significant antitrust concerns.

The final rule is not effective until mid-January, 2025 (90-days after publication in the Federal Register), assuming it is not enjoined by a court prior to that date. The FTC's Premerger Notification Office plans to issue further compliance guidance before the final rule's effective date.

Crowell & Moring is closely following all developments on these issues and will provide further updates. Please reach out to your C&M contact for further information or if you have any questions.

Contacts

Insights

Client Alert | 9 min read | 08.02.26

The 2026 ICC Arbitration Rules: A New Era

The International Chamber of Commerce (ICC) has released its revised 2026 Arbitration Rules (the 2026 Rules), which entered into force on 1 June 2026. The 2026 Rules apply to any arbitration commenced on or after 1 June 2026, unless the parties have agreed otherwise. The revisions were driven by increased competition among arbitral institutions—illustrated by recent amendments to the Singapore International Arbitration Centre (SIAC) Rules in August 2025 and the anticipated update to the London Court of International Arbitration (LCIA) Rules.

Client Alert | 4 min read | 07.31.26

Client Alert | 3 min read | 07.31.26

Client Alert | 5 min read | 07.28.26

Data Centers in the Crosshairs: The Plaintiffs' Bar Has Begun Filing New Claims Using Old Tricks